Keeping an eye on our credit reports is an important part of protecting our financial health. Federal law gives us the right to access free Credit Reports, and reviewing them regularly can help us catch errors, detect identity theft, and avoid problems when applying for a credit card, mortgage, vehicle loan, or student loan.

At Fair Credit Attorneys, we help consumers understand their rights under the Fair Credit Reporting Act and take action when credit reporting agencies fail to report accurate information. If credit report errors are hurting your credit score or causing a credit report denial, our team is here to help. Contact us today for a free consultation.

Understanding Credit Reports

A credit report is a detailed record of our borrowing history. Credit reporting companies collect information from lenders and financial institutions to build our credit file.

A typical credit report includes:

- Personal information

- Credit card accounts

- Account balances

- Bill payment history

- Vehicle loans and student loans

- Medical debt

- Bankruptcy history

- Credit inquiries and collections

These details are used by credit reporting bureaus like Equifax, Experian, and TransUnion to help determine our Credit Scores. Those scores affect mortgage rates, credit card approvals, and even rental applications.

Who Is Entitled to Free Credit Reports?

Thanks to federal law and the Fair Credit Reporting Act, every consumer has the right to access their Credit Reports for free under certain conditions.

The Federal Trade Commission oversees consumer protections and helps regulate consumer reporting companies to ensure accuracy and fairness.

Free credit reports help us:

- Monitor our financial health

- Detect identity theft early

- Improve our credit score

- Prepare for major financial decisions

- Identify errors in our credit history

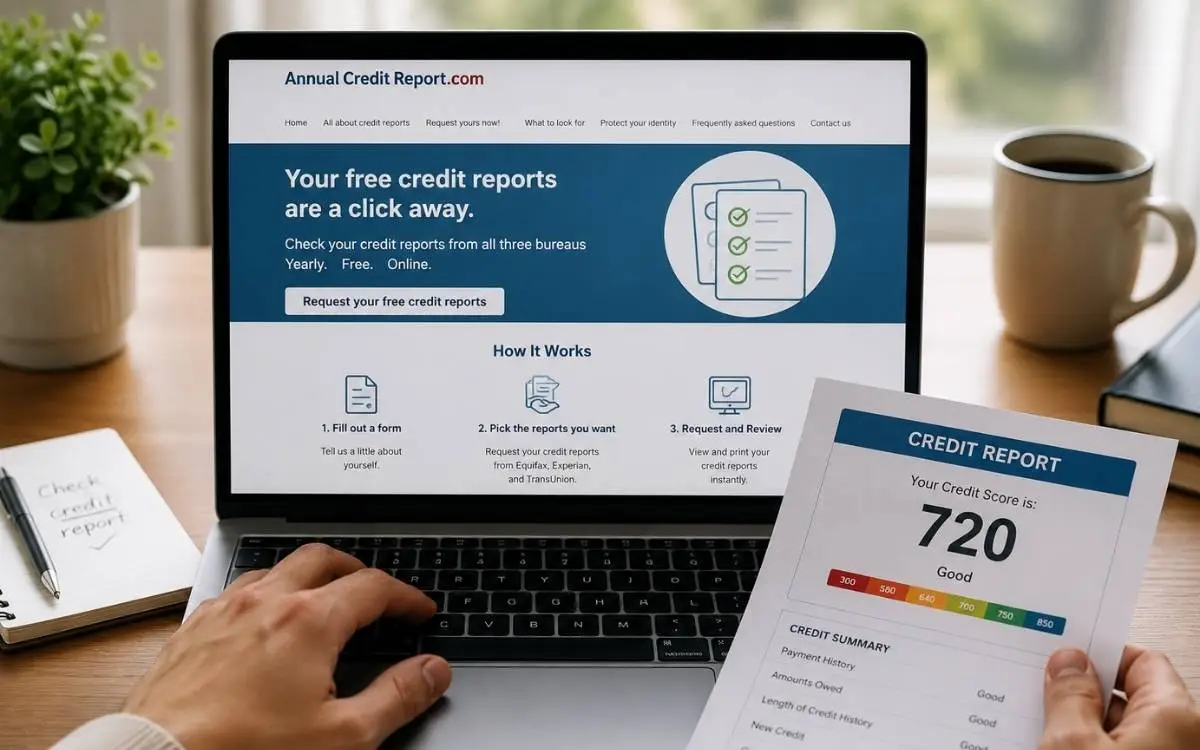

How to Get Your Free Credit Report Through AnnualCreditReport.com

We can get free Credit Reports through AnnualCreditReport.com, the only website authorized by federal law to provide reports from Equifax, Experian, and TransUnion.

The process is simple and usually takes only a few minutes. We may need to verify our identity using basic information like:

- Name and address

- Date of birth

- Social Security number

Once verified, we can access our credit report data from each credit reporting bureau and review it for errors, suspicious activity, or signs of identity theft.

Checking all three reports is important because each credit reporting agency may show different information. Regular reviews help protect our financial health, improve our credit score, and support better outcomes for credit card approvals, loans, and mortgage rates.

If we find mistakes, Fair Credit Attorneys can help us take action under the Fair Credit Reporting Act and work to correct inaccurate information.

Why We Should Review All Three Credit Reports

Each credit reporting bureau may contain different information. One report may show outdated accounts, while another may contain incorrect balances or missing payment history.

When we review all three reports, we can catch issues such as:

- Incorrect account balances

- Missing payment history

- Duplicate accounts

- Outdated collections

- Errors affecting Credit Scores

Situations That May Qualify Us for Additional Free Reports

In some cases, we may be entitled to additional free Credit Reports beyond the annual free report.

After an Adverse Action

If we are denied credit, housing, or loans based on our credit file, we may receive an adverse action notice. This allows us to request another free report to review what affected the decision.

After Identity Theft

If we are victims of identity theft, we may need to check our reports more frequently to monitor unauthorized accounts or suspicious activity.

Signs of Identity Theft

Early detection is critical. Common signs include:

- Accounts we do not recognize

- Suspicious activity on credit cards

- Unexpected collections

- Credit report denial without clear reason

- Unknown inquiries on our credit file

How We Can Protect Ourselves

We have several tools available to help prevent fraud and protect our personal financial information.

Fraud Alerts

A fraud alert warns lenders to verify identity before opening new accounts.

Credit Freeze

A credit freeze restricts access to our credit file, preventing new accounts from being opened.

Credit Monitoring

Credit monitoring services track changes in our credit report and alert us to suspicious activity.

What Errors Should We Look For?

Credit reports often contain mistakes that can impact our financial life. We should carefully review for:

- Incorrect personal information

- Accounts that do not belong to us

- Incorrect payment history

- Wrong account balances

- Medical debt errors

- Bankruptcy history mistakes

- Duplicate accounts

Even small errors can negatively affect our credit score and financial opportunities.

Learn More: Examples of credit report errors

How Credit Report Errors Can Hurt Us

Inaccurate credit information can lead to serious financial consequences, including:

- Higher mortgage rates

- Difficulty obtaining vehicle loans

- Problems qualifying for student loans

- Higher insurance costs

- Credit card denials

- Rental application issues

- Reduced access to good credit opportunities

How to Dispute Errors on Our Credit Report

If we find incorrect information, we have the right to dispute it.

Step 1: Gather Documentation

We should collect evidence such as account statements or payment records.

Step 2: File a Dispute

We can submit disputes to credit reporting agencies and the company that provided the information.

Step 3: Investigation

Under the Fair Credit Reporting Act, credit reporting companies must investigate and correct inaccurate data when supported by evidence.

Learn More: How to fix credit report errors

Identity Theft Reports and Recovery

If we are victims of identity theft, filing an Identity Theft Report can help us begin recovery.

We may also need to:

- Place fraud alerts

- Freeze credit reports

- Close fraudulent accounts

- Monitor financial accounts closely

These steps help limit further damage to our financial health.

When Credit Reporting Violations May Occur

Sometimes credit reporting agencies fail to follow the law. Violations may include:

- Failing to properly investigate disputes

- Reporting incorrect or outdated information

- Mixing files between consumers

- Ignoring evidence of inaccuracy

- Continuing to report disputed data

These actions may violate the Fair Credit Reporting Act and can seriously harm our credit history.

When to Contact Fair Credit Attorneys

If inaccurate information remains on our credit reports after disputes, legal help may be necessary.

At Fair Credit Attorneys, we help clients dealing with:

- Identity theft

- Credit reporting errors

- Damaged credit scores

- Mixed credit files

- Unresolved disputes with credit reporting agencies

- Wrongful credit report denial

We work to hold credit reporting companies accountable and help restore accuracy to your credit file.

Conclusion

Getting free Credit Reports is one of the most effective ways to protect our financial future. By reviewing our reports regularly, we can catch errors, detect identity theft early, and maintain strong financial health.

If inaccurate information is hurting your credit score or affecting your ability to get credit card approvals, loans, or better mortgage rates, Fair Credit Attorneys can help. We use the protections under the Fair Credit Reporting Act to fight inaccurate reporting and help restore your financial standing. Call us today at (866) 381 6444 for a free consultation.

Frequently Asked Questions

Does checking my credit report hurt my credit score?

No. Checking your own credit report does not affect your credit score.

How often should I check my credit reports?

At least once per year, but more often if we suspect fraud or are rebuilding credit.

Why are my credit reports different?

Each credit reporting bureau receives information from different lenders, so data may vary.

What should I do if I see fraud?

Immediately place a fraud alert or credit freeze and dispute the accounts.